Market Size: USD 16.4 Billion in 2024, Forecasting USD 33.0 Billion by 2030

The Saudi Green Building market is entering a transformative phase, with revenues projected at USD 16.4 billion in 2024 and expected to nearly double to USD 33.0 billion by 2030. This expansion reflects a 12.3% CAGR over the forecast period, underscoring the Kingdom’s commitment to sustainable construction. The surge is driven by rapid urbanization, population growth, and a national pivot toward energy-efficient infrastructure.

Riyadh Leads with 40% Share and Fastest Growth Rate of 12.6%

Among Saudi provinces, Riyadh dominates with 40% of the market share in 2024 and is also the fastest-growing region, expanding at a 12.6% CAGR. As the country’s financial and business hub, Riyadh is spearheading large-scale projects that align with Vision 2030 and the Saudi Green Initiative. This dual role as both the largest and fastest-growing province highlights its centrality in shaping the future of Saudi Green Building adoption.

Roofing Holds the Largest Application Share, While Insulation Grows Fastest at 12.8%

Applications of green building materials reveal a split between scale and speed. Roofing remains the largest category, reflecting the demand for durable, climate-adapted solutions. Meanwhile, insulation is the fastest-growing segment, with a CAGR of 12.8%, as the desert climate necessitates advanced thermal regulation. Materials such as mineral wool, cellulose, hemp, and straw bales not only insulate but also provide fire, insect, and fungal resistance, making them indispensable in Saudi construction.

Bamboo Dominates with 30% Share; Sustainable Wood Expands at 12.7% CAGR

Material preferences in the Saudi Green Building market highlight a balance between tradition and innovation. Bamboo accounts for 30% of the market in 2024, favored for its elasticity, durability, and low energy production footprint—11.5 times less than steel and 45 times less than aluminum. On the other hand, sustainable wood is the fastest-growing material, with a CAGR of 12.7%, thanks to its acoustic properties, recyclability, and potential for reuse or conversion into biofuel. Together, these materials illustrate how Saudi Arabia is blending ecological responsibility with structural performance.

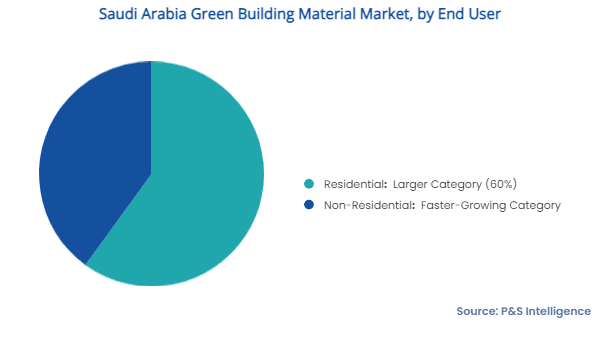

Residential Holds 60% Share, While Non-Residential Expands Faster

In terms of end users, residential projects account for 60% of the market, reflecting the scale of housing demand. However, non-residential construction is growing faster, fueled by government-backed initiatives such as the Saudi Green Initiative (SGI) and Vision 2030. These programs emphasize eco-friendly commercial and institutional projects, from energy parks to business complexes, ensuring that sustainability is embedded into the nation’s economic diversification strategy.

Regulations and Certifications Strengthen Saudi Green Building Adoption

Policy frameworks are playing a decisive role in shaping the Saudi Green Building market. The MOSTADAM certification and the Saudi Green Building Code (SgBC 1001) mandate sustainable practices, ensuring that new projects minimize ecological footprints. Additionally, flagship developments like King Salman Energy Park (SPARK), which achieved LEED Silver certification, showcase how international standards are being integrated into Saudi Arabia’s construction landscape.

Market Fragmentation Creates Opportunities for Innovation

The Saudi Green Building market is fragmented, with multiple players focusing on roofing, insulation, and framing materials. Companies such as Saudi Ceramic Co., Saudi Readymix Concrete Co., Saveto Group, Attieh Steel Ltd., and Edama Organic Solution are actively shaping the competitive landscape. This fragmentation fosters innovation, as firms experiment with recycled metals, hempcrete, and bio-concrete additives to meet sustainability goals.

Recycling in Makkah: SAR 113 Million Annual Potential

A striking example of the market’s economic-environmental synergy comes from Makkah. Recycling construction materials there could prevent 5.6 tons of methane emissions annually, equivalent to 140.1 thousand mtCO2e, while generating SAR 113 million in net revenue. This dual benefit of environmental protection and economic gain illustrates why Saudi Green Building practices are becoming central to national policy.

Outlook: Saudi Green Building as a Pillar of Vision 2030

Looking ahead, the Saudi Green Building market is poised to become a cornerstone of the Kingdom’s sustainable development agenda. With strong government backing, rapid material innovation, and rising demand for both residential and non-residential projects, the sector is set to deliver not only environmental benefits but also long-term economic resilience. By 2030, the market’s projected USD 33.0 billion valuation will reflect not just growth, but a redefinition of how Saudi Arabia builds for the future.

Also Read: Saudi Smart Construction Drives 6.2% Sector Growth

Frequently Asked Questions (FAQs) on the Saudi Green Building Market

Q1. What is the current size of the Saudi Green Building market?

The Saudi Green Building market is valued at USD 16.4 billion in 2024 and is projected to reach USD 33.0 billion by 2030, growing at a 12.3% CAGR.

Q2. Which province leads the Saudi Green Building market?

Riyadh holds the largest share at 40% in 2024 and is also the fastest-growing province, expanding at a 12.6% CAGR during the forecast period.

Q3. What are the main applications of Saudi Green Building materials?

The largest application is roofing, while insulation is the fastest-growing segment with a 12.8% CAGR, driven by the need for thermal regulation in Saudi Arabia’s desert climate.

Q4. Which materials dominate the Saudi Green Building market?

Bamboo leads with 30% of the market in 2024, thanks to its durability and low energy production footprint. Sustainable wood is the fastest-growing material, expanding at 12.7% CAGR due to its recyclability and acoustic benefits.

Q5. Who are the key players in the Saudi Green Building industry?

Major companies include Saudi Ceramic Co., Saudi Readymix Concrete Co., Saveto Group, Attieh Steel Ltd., Al Kuhaimi Group Holding, and Edama Organic Solution.

Q6. What role do regulations play in Saudi Green Building adoption?

Government initiatives such as the MOSTADAM certification and the Saudi Green Building Code (SgBC 1001) mandate sustainable construction practices, ensuring reduced ecological footprints.

Q7. Which end-user segment is growing fastest?

While residential projects account for 60% of the market, the non-residential sector is expanding faster, supported by Vision 2030 and the Saudi Green Initiative.

Q8. How does recycling contribute to the Saudi Green Building market?

Recycling construction materials in Makkah could prevent 5.6 tons of methane emissions annually and generate SAR 113 million in net revenue, showcasing the dual benefits of sustainability and economic growth.