Demand for cement in the Kingdom is growing, driven by major development plans. Technavio forecasts the Saudi Arabia cement market size will increase by USD 2.57 billion at a CAGR of 6.4% from 2025 to 2030. At the same time, sustainability is moving from a side topic to a core supply issue. That tension is at the heart of low carbon cement Saudi Arabia efforts.

Saudi cement also matters for emissions. A life cycle assessment paper notes an annual cement production capacity of 75 Mt in 2022. It also reports the Saudi cement industry accounted for about 9% of the nation’s stationary CO₂ emissions in 2022, equal to 36.2 Mt/year. The same source highlights a clinker-to-cement ratio (CTC) of 0.90–0.95, plus strong reliance on oil (Arab light) and heavy fuel oil (HFO) for thermal and electrical energy generation.

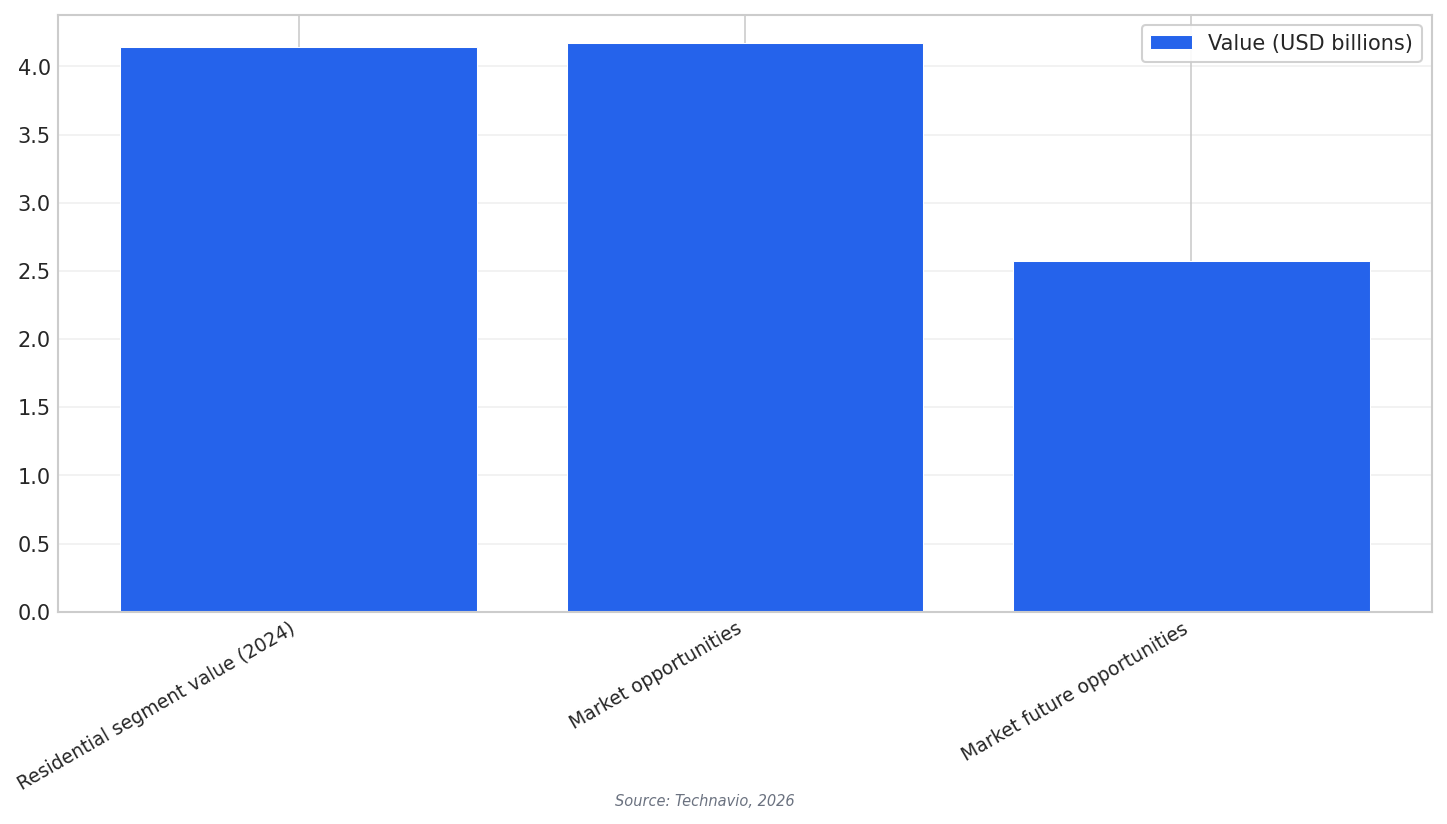

Key market figures show where supply pressure is strongest. Technavio reports the residential segment was valued at USD 4.14 billion in 2024. It also lists market opportunities of USD 4.17 billion and market future opportunities of USD 2.57 billion, all in USD billions.

How CCUS and SCMs Change the Concrete Supply Chain

Technavio describes a strategic shift toward sustainability, including carbon capture utilization technologies and more supplementary cementitious materials (SCMs) to lower the carbon footprint. The life cycle assessment paper also lists strategies used globally: alternative fuels, better kiln efficiency, decarbonizing thermal and electrical energy, reducing clinker content with SCMs, and deploying carbon capture and storage (CCS). In simple terms, CCUS targets CO₂ after it is made, while SCMs reduce how much clinker is needed in the first place.

In Saudi Arabia, the path is not only technical. IMD reports that standards for what qualifies as green cement are still under development. Emissions reporting is not yet mandatory. It also notes most public tenders continue to prioritize price over environmental performance. City Cement’s CEO describes a “credibility gap” where people want sustainable cement, but they want proof and do not always want to pay more.

Material availability is another practical limit. A PR Newswire release says imported SCMs such as fly ash or GGBFS are often unavailable at scale in Saudi Arabia. It describes a low-carbon, CNT-enhanced concrete demonstration in Dammam using two adjacent 4X4 meter concrete pads, one CNT mix and one control mix. The same release notes Saudi Readymix was founded in 1978 and has supplied over 100 million m³ of concrete, showing how large ready-mix supply networks can be in the Kingdom.

Why is low carbon cement Saudi Arabia hard to scale today?

What are the main levers mentioned for cutting cement emissions?

What do the sources say about Saudi cement’s emissions footprint?

Are supplementary cementitious materials always easy to source in Saudi Arabia?

Talk to us for your needs in:

-

Sustainable Construction Solutions

-

Strategic Construction Planning

-

Customer-Centric Construction Services

-

Operational Excellence in Construction

-

Leadership and Change Management for Construction

-

Digital Transformation in Construction

-

Saudi Construction Market Research

-

In-Depth Market Study for Construction

-

Market Intelligence and Insights in Construction

-

Feasibility Study and Assessment in Construction

-

Saudi Construction Benchmarking