Flood risk is no longer a side issue for insurers. One source says flood losses have “inundated re/insurers’ claims books,” turning a so-called “secondary” peril into a primary concern. In Saudi Arabia, that matters for construction sites, temporary works, and critical infrastructure that can be exposed in a single event. The 2025–2026 flood backdrop also arrives as the local insurance market is expanding fast, but protection is still not deep enough.

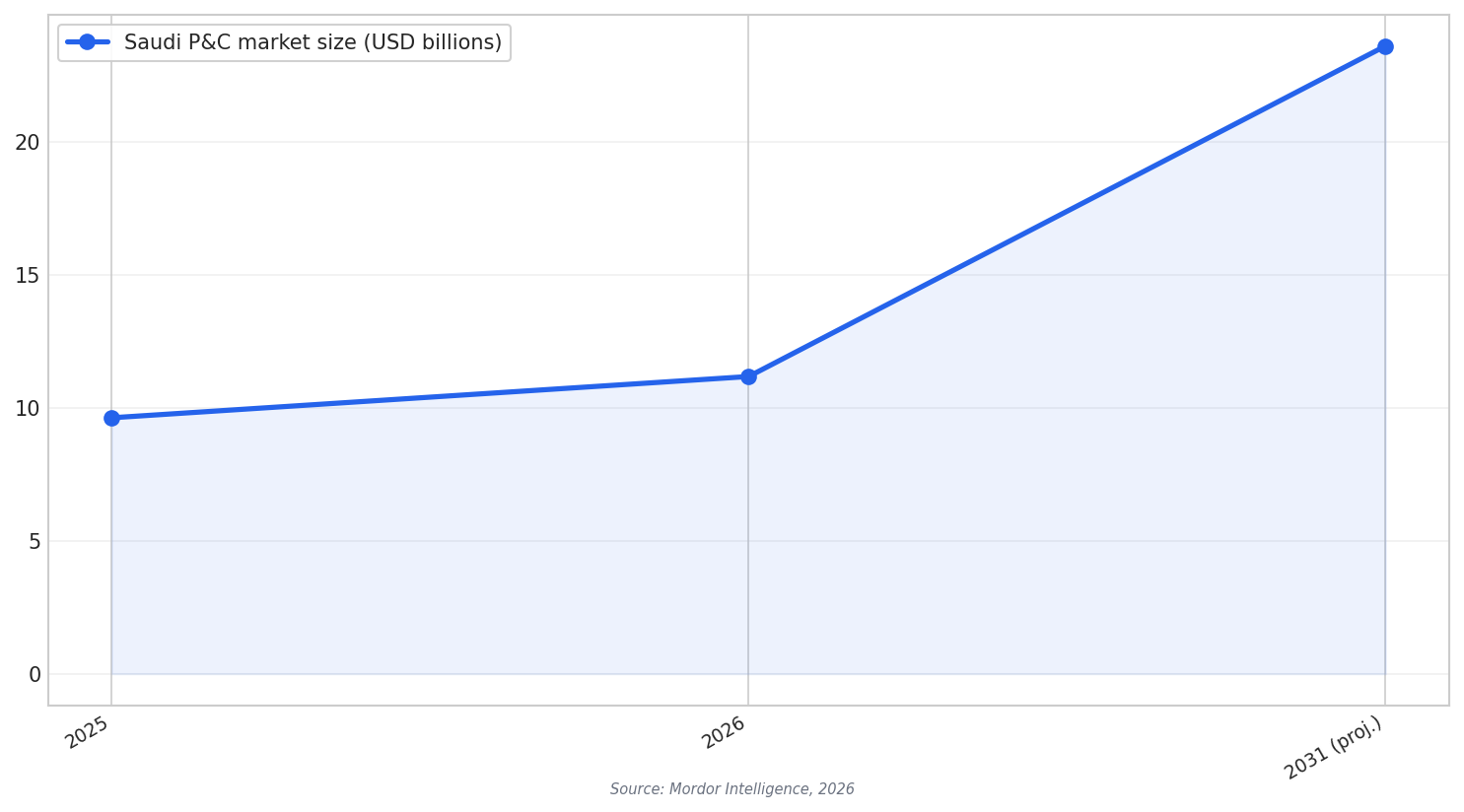

Market figures show why the discussion is urgent. Mordor Intelligence estimates Saudi Arabia’s property and casualty insurance market at USD 9.62 billion in 2025 and USD 11.17 billion in 2026, with a projection of USD 23.59 billion by 2031. The same report says penetration remains low at 1.5%, which points to a protection gap. For builders and project owners, low penetration can mean uneven risk awareness and inconsistent buying of robust construction covers.

The chart below summarizes these three market-size data points: USD 9.62 billion (2025), USD 11.17 billion (2026), and USD 23.59 billion (2031 projection). These figures frame the scale of premium at stake when flood losses hit large projects and many policies respond at once.

Flood gaps are not only a Saudi issue, and that is useful context when reviewing construction all risk insurance Saudi Arabia. One industry note cites a “$255 billion flood protection gap” and says that in the last five years flooding caused an estimated $325 billion in global economic losses, yet only $70 billion was insured (attributed to Munich Re in that source). When economic loss and insured loss diverge, contract wording and sub-limits get tested, and projects can discover that “all risk” does not always mean “all outcomes are paid.”

Where 2025–2026 Flood Pressure Can Expose CAR Weak Spots

Construction all risk insurance is often bought for big sites, but flood can still produce disputes if the risk view is weak at placement. Better flood intelligence can help. Fathom describes “highly granular Risk Scores” that can feed pricing tools and generate a technical price, delivered “in under a second” via an API. It also emphasizes understanding aggregations fast, which matters when multiple sites sit in the same drainage basin or coastal zone and a single storm triggers many claims.

Stress testing is another area that can reveal gaps early, before a flood. Fathom’s Climate Dynamics framework is described as supporting flood-risk views across global warming levels “to 5°C” and time horizons “to 2100,” using an ensemble of climate models to quantify uncertainty. Separately, a 2026 Sustainability paper focused on Eastern Saudi Arabia highlights that sea-level rise and coastal flooding are pressing challenges, intensified by rapid urbanization, and can damage critical infrastructure. Together, these sources support a simple lesson: CAR programs need clear flood assumptions, site-by-site evaluation, and portfolio-level aggregation checks.

Why did 2025–2026 floods raise concern about construction all risk insurance Saudi Arabia?

What numbers show the Saudi insurance market context around these flood events?

How big is the global flood protection gap in the provided sources?

How can insurers and brokers tighten flood decisions for construction risks?