Saudi Arabia’s building cycle sits inside a wider GCC construction boom that is pushing steel demand across residential, commercial, and industrial projects. One source notes urban population growth averaging 3.2% annually across GCC countries, and links this growth to heavy investment in housing projects, shopping centers, and mixed-use developments. The same source ties demand to major project pipelines by citing NEOM as an example of where machine learning is used for real-time demand forecasting. At the same time, the shift toward sustainable construction practices is increasing interest in high-strength, lightweight steel products and “environmentally friendly production methods.” These forces shape how green steel Saudi Arabia construction supply conversations are evolving, even when supply is regional rather than purely domestic.

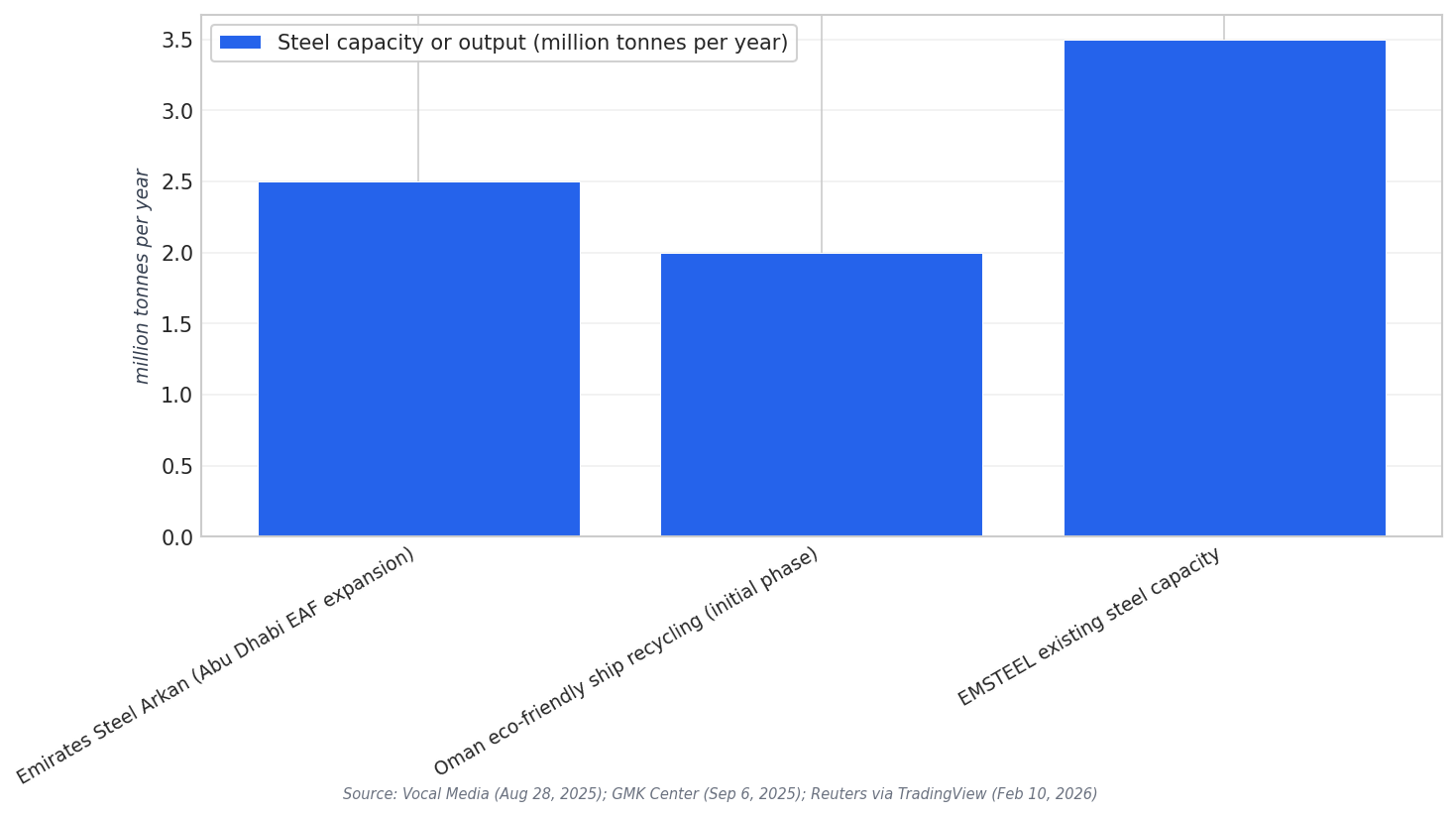

On the supply side, the new EAF capacity pipeline in the region includes a major announced expansion in Abu Dhabi. In June 2025, Emirates Steel Arkan announced a $1.2 billion expansion of its Abu Dhabi facility, adding electric arc furnace capacity to increase production by 2.5 million tons annually and reduce carbon emissions by 30%. That single announcement matters for Saudi buyers because it adds incremental long-product availability within the Gulf, and it is directly framed as an emissions-reduction move. Separately, Oman announced construction of an integrated eco-friendly ship recycling facility, with an initial phase output of around 2 million tons of high-quality low-carbon steel per year. Together, these projects show more EAF-linked and recycling-linked supply options coming into the same neighborhood as Saudi construction procurement.

What “Green” Signals Look Like in GCC Long Products

Demand for low-carbon and fully traceable steel is rising in the UAE as regulators tighten standards, according to Fastmarkets reporting from November 2025. That same report includes an on-the-ground demand marker: monthly UAE rebar demand grew from 350,000 tonnes in January to 500,000 tonnes in November. Arabian Gulf Steel Industries (AGSI) positions “Net-Zero Steel” around a fully electric route using 100% locally recycled raw materials, without iron ore, coke, or other high-emitting blast furnace inputs. AGSI’s installed capacity is listed as 720,000 tonnes of billet, 960,000 tonnes of rebar, and 240,000 tonnes of sections, yet AGSI estimates it can meet only about 15% of the UAE’s long-product demand with certified Net-Zero Steel. For Saudi construction, this highlights a practical constraint: certification-focused supply can be a subset of the broader tonnage requirement.

Large integrated producers are also building credibility around greener practices and energy security. Reuters reporting published on TradingView states that EMSTEEL operates 14 state-of-the-art plants with production capacity of 3.5 million tonnes of steel and 4.6 million tonnes of cement annually. The same source notes a 20-year natural gas supply agreement with ADNOC Gas valued between USD3.5 and USD4.2 billion, effective from January 2027, aimed at underpinning operations and future growth. EMSTEEL also launched the world’s first Electric Process Gas Heater (ePGH) pilot in steelmaking, replacing gas-fired heaters with an electric alternative at its DRI plants and eliminating over 2,200 tonnes of CO₂ annually. It delivered the region’s first hydrogen-based rebar for Abu Dhabi’s first net-zero carbon mosque by Aldar in Sustainable City, Yas Island, and became the first company in MENA to earn ResponsibleSteel™ certification.

For Saudi construction buyers thinking about “green steel” supply, the near-term outlook in the sources is shaped more by GCC-adjacent capacity additions and certified-product availability than by detailed Saudi mill-by-mill disclosures. The regional picture includes EAF expansion adding 2.5 million tons annually in Abu Dhabi, low-carbon steel output of around 2 million tons per year planned in Oman’s ship-recycling pathway, and a UAE market where rebar demand moved from 350,000 to 500,000 tonnes per month across the year. Meanwhile, the same GCC market source highlights automation and smart furnaces reducing energy consumption by 15%, and digital twins and IoT sensors improving operational efficiency by 20% across GCC facilities. The practical takeaway is that green steel procurement for Saudi projects may increasingly depend on cross-border supply planning, certification availability, and electrified or recycling-based routes that can be documented and traced.

What does “green steel Saudi Arabia construction supply” mean in this article?

What new EAF-linked capacity is highlighted in the sources?

What low-carbon steel output is planned from Oman’s ship recycling project?

What does Fastmarkets report about UAE rebar demand?

What green-steel milestones are attributed to EMSTEEL in the sources?